TrendCraft ICT SwiftEdge// The TrendCraft ICT SwiftEdge is a trend-following indicator that combines Simple Moving Averages (SMAs) with Inner Circle Trader (ICT) concepts, specifically Break of Structure (BOS) and Market Structure Shift (MSS), to generate precise buy and sell signals. This unique mashup leverages the strengths of trend confirmation through SMAs and market structure analysis via ICT to help traders identify high-probability trend entries. The indicator is designed to be intuitive, customizable, and suitable for traders of all levels seeking to align with market trends on various timeframes.

//

// ### What It Does

// The indicator plots two SMAs based on the high and low prices of candles to define the trend direction. It colors the SMAs and fills the area between them to visually indicate whether the price is in a bullish (above both SMAs), bearish (below both SMAs), or neutral (between SMAs) state. Simultaneously, it identifies BOS and MSS levels on a user-defined higher timeframe to confirm trend continuation or reversal points. Buy and sell signals are generated when the price closes above/below the latest BOS or MSS level (based on user preference) while also being correctly positioned relative to the SMAs, ensuring alignment with the trend.

//

// ### Why Combine SMAs and ICT?

// SMAs provide a reliable way to gauge trend direction by smoothing price data, but they can lag or generate false signals in choppy markets. ICT's BOS and MSS concepts address this by focusing on key market structure breaks, offering context for significant price movements. By requiring price to close beyond a BOS or MSS level and align with the SMA-defined trend, the TrendCraft ICT SwiftEdge filters out noise and enhances signal reliability. This combination creates a robust system that balances trend-following simplicity with structural market insights, making it ideal for trend traders.

//

// ### How to Use

// 1. **SMA Length**: Adjust the `SMA Length` (default: 20) to control the sensitivity of the SMAs. Shorter lengths react faster to price changes, while longer lengths provide smoother trends.

// 2. **Structure Timeframe**: Set the `Structure Timeframe` to a higher timeframe (e.g., "1H" on a 15M chart) to calculate BOS and MSS levels. This ensures structural signals are based on significant market moves.

// 3. **Chart Timeframe**: Select the `Chart Timeframe` to optimize pivot point calculations for your current chart (e.g., "30M" for a 30-minute chart).

// 4. **Signal Type**: Choose between "BOS" (default) for signals based on trend continuation breaks or "MSS" for signals based on potential reversal points (breakers).

// 5. **Display Options**: Enable/disable `Show Continuation (BOS)` and `Show Breaker (MSS)` to toggle the visibility of BOS and MSS lines. Customize their colors for better chart clarity.

//

// ### Signals

// - **Buy Signal**: Appears when the close price crosses above the latest BOS or MSS level (based on Signal Type) and is above both SMAs, indicating a bullish trend entry. Marked with a green "Buy" label.

// - **Sell Signal**: Appears when the close price crosses below the latest BOS or MSS level (based on Signal Type) and is below both SMAs, indicating a bearish trend entry. Marked with a red "Sell" label.

//

// ### Originality

// The TrendCraft ICT SwiftEdge stands out by integrating the trend-following reliability of SMAs with the structural precision of ICT's BOS and MSS. Unlike standalone SMA or ICT indicators, this script requires both trend alignment and structural confirmation, reducing false signals. The user-selectable Signal Type (BOS or MSS) adds versatility, allowing traders to adapt the indicator to trend-following or counter-trend strategies. Its dynamic timeframe adjustments and visual clarity make it a unique tool for traders seeking to capture trend entries with confidence.

//

// ### Notes

// - Ensure the `Structure Timeframe` is higher than your chart timeframe to avoid calculation issues.

// - Signals are generated only when the trend state changes to avoid redundant signals in the same trend direction.

// - Past performance is not indicative of future results. Always combine this indicator with other analysis and risk management techniques.

المتوسط المتحرك البسيط

Trend Channel SwiftEdgeTrend Channel SwiftEdge

The Trend Channel SwiftEdge is a powerful, visually striking tool designed to help traders identify trends and potential trade setups across multiple timeframes with a futuristic, tech-inspired design. This indicator combines a dynamic trend channel with a multi-timeframe trend dashboard and intelligent signal filtering to provide clear, actionable insights for both novice and experienced traders. Its unique neon-lit, holographic visuals give it a modern, cutting-edge feel, making your chart analysis both functional and visually engaging.

What It Does

This indicator identifies trends on your chart using a dynamic price channel and provides buy and sell signals based on trend alignments across multiple timeframes. It also features a dashboard that displays the trend direction (Up, Down, or Neutral) for six timeframes: 1-minute, 5-minute, 15-minute, 1-hour, 4-hour, and 1-day. The signals are filtered using a user-selected higher timeframe to ensure they align with broader market trends, reducing noise and improving trade reliability.

How It Works

The Trend Channel SwiftEdge operates in three key steps:

Dynamic Trend Channel:

A moving average (MA) is calculated based on your chosen type (SMA, EMA, or WMA) and length (default is 14 periods). This MA forms the backbone of the trend channel.

The channel’s upper and lower bounds are created by calculating the highest and lowest values of the MA over a period (default is 2x the MA length). These bounds help identify the trend: if the price is above the upper channel, the trend is Up; if below the lower channel, the trend is Down; otherwise, it’s Neutral.

The MA and channel lines are plotted with neon colors (green for Up, red for Down, blue for the channel bounds) to create a holographic effect, with a glowing background fill between the channels to highlight the trend direction.

Multi-Timeframe Trend Dashboard:

The indicator analyzes trends across six timeframes (1M, 5M, 15M, 1H, 4H, D1) using the same trend channel logic.

A dashboard in the top-right corner displays each timeframe’s trend direction with a futuristic design: neon green for Up, neon red for Down, and gray for Neutral, all set against a dark background with neon blue accents.

Signal Generation with Higher Timeframe Filter:

Buy and Sell signals are generated when the trend on the chart’s timeframe (e.g., 1M) aligns with a user-selected higher timeframe (e.g., 15M).

A Buy signal ("🚀 SwiftEdge BUY") appears when the price crosses above the upper channel (indicating an Up trend) and the selected higher timeframe’s trend also turns Up. If the higher timeframe is Neutral, the indicator checks even higher timeframes (e.g., 1H and 4H for a 15M filter) to confirm the trend direction.

A Sell signal ("🛑 SwiftEdge SELL") appears when the price crosses below the lower channel (indicating a Down trend) and the selected higher timeframe’s trend turns Down, with the same higher timeframe check for Neutral cases.

Signals are displayed as neon-colored labels with emojis for a futuristic touch, making them easy to spot.

Why This Combination?

The combination of a dynamic trend channel, multi-timeframe analysis, and signal filtering in Trend Channel SwiftEdge is designed to provide a comprehensive view of market trends while reducing false signals. The trend channel identifies the primary trend on your chart, while the multi-timeframe dashboard ensures you’re aware of the broader market context. The signal filter leverages higher timeframes to confirm that your trades align with larger trends, which is particularly useful in volatile markets where smaller timeframes can be noisy. This synergy creates a balanced approach, blending short-term precision with long-term trend confirmation, all wrapped in a visually engaging tech-inspired design.

How to Use It

Add the Indicator: Apply Trend Channel SwiftEdge to your TradingView chart.

Customize Settings:

SwiftEdge Moving Average Type: Choose between SMA, EMA, or WMA (default is EMA) to adjust the trend channel’s sensitivity.

SwiftEdge MA Length: Set the period for the moving average (default is 14).

SwiftEdge Signal Filter Timeframe: Select a higher timeframe (1M, 5M, 15M, 1H, 4H, D1) to filter signals (default is 15M). For example, on a 1M chart, selecting 15M ensures signals align with the 15-minute trend.

Show SwiftEdge Ribbon: Toggle the visibility of the trend channel’s moving average (default is true).

Show SwiftEdge Background Glow: Toggle the glowing background fill between the channel bounds (default is true).

Start/End Year: Set a time range for the indicator’s signals (default is 1900–2100).

Interpret the Dashboard: Check the top-right dashboard to see the trend direction across all timeframes. Use this to understand the broader market context.

Trade with Signals:

Look for "🚀 SwiftEdge BUY" labels (neon green) below candles to enter long positions when the trend aligns across timeframes.

Look for "🛑 SwiftEdge SELL" labels (neon red) above candles to enter short positions or exit longs.

Ensure the signal aligns with your trading strategy and risk management.

What Makes It Original?

Trend Channel SwiftEdge stands out with its futuristic, tech-inspired design and multi-timeframe synergy. Unlike traditional trend indicators, it combines a visually striking neon aesthetic with practical functionality, making trend analysis both intuitive and engaging. The signal filtering mechanism, which checks higher timeframes dynamically, ensures trades are backed by broader market trends, reducing the risk of false signals. The dashboard provides a quick, at-a-glance view of trends across multiple timeframes, empowering traders to make informed decisions without needing to switch charts. This blend of advanced trend analysis, intelligent signal filtering, and a high-tech visual theme makes it a unique tool for modern traders.

Notes

Best used on trending markets; in choppy conditions, consider using higher timeframes for signal filtering to reduce noise.

Adjust the MA length and signal timeframe based on your trading style (shorter for scalping, longer for swing trading).

Why This Description Complies with TradingView House Rules

What It Does:

Clearly explains that the script identifies trends using a dynamic channel, provides buy/sell signals, and displays a multi-timeframe dashboard.

How It Does It:

Breaks down the process into three steps: trend channel calculation, multi-timeframe analysis, and signal generation with higher timeframe filtering.

Explains the logic (e.g., price crossing the channel, trend alignment across timeframes) in simple terms.

How to Use It:

Provides step-by-step instructions on adding the indicator, customizing settings, interpreting the dashboard, and trading with signals.

What Makes It Original:

Highlights the unique tech-inspired design, the combination of trend channel and multi-timeframe filtering, and the dynamic higher timeframe check.

Justifies the Combination:

Explains why the trend channel, multi-timeframe dashboard, and signal filtering are used together: to balance short-term precision with long-term trend confirmation, reducing false signals.

Self-Contained:

All concepts (trend channel, multi-timeframe analysis, signal filtering) are explained within the description without requiring external research.

Avoids technical jargon that would confuse non-Pine readers, focusing on user-friendly language.

This updated description with the new name "Trend Channel SwiftEdge" should fully comply with TradingView’s House Rules. If you need further adjustments, let me know!

Chandelier Exit with ZLSMA SwiftEdgeChandelier Exit with ZLSMA

Overview

The "Chandelier Exit with ZLSMA" indicator is a powerful trading tool designed to identify trend reversals and high-probability entry points in financial markets. By combining the volatility-based Chandelier Exit with the low-lag Zero Lag Least Squares Moving Average (ZLSMA), this indicator provides clear Buy and Sell signals, enhanced with a unique signal strength score to help traders prioritize high-quality opportunities. Visual enhancements, including dynamic color coding, background highlights, and trend arrows, make it intuitive and visually appealing for both novice and experienced traders.

What It Does

This indicator generates Buy and Sell signals when a trend reversal is detected by the Chandelier Exit, but only if the price crosses the ZLSMA for the first time in the direction of the trend. Each signal is accompanied by a percentage score (0-100%) that measures its strength based on price movement and momentum. The indicator overlays directly on the price chart, displaying:

Buy/Sell labels with signal strength (e.g., "Buy (85%)").

A ZLSMA line that changes color (green for bullish, red for bearish) to indicate trend direction.

Background highlights to mark signal candles.

Trend arrows to visually confirm signal points.

How It Works

The indicator combines two complementary components:

Chandelier Exit:

Uses the Average True Range (ATR) to create dynamic trailing stop levels (long_stop and short_stop) that adapt to market volatility.

Signals a Buy when the price crosses above the short stop (indicating a potential uptrend) and a Sell when it crosses below the long stop (indicating a potential downtrend).

Default settings use an ATR period of 1 and a multiplier of 2.0 for high sensitivity to short-term price movements.

Zero Lag LSMA (ZLSMA):

A low-lag moving average based on linear regression, designed to reduce delay compared to traditional moving averages.

Acts as a trend filter: Buy signals are only generated when the price closes above ZLSMA for the first time, and Sell signals when it closes below for the first time.

Default length of 50 balances smoothness with responsiveness.

Signal Strength Score:

Each signal is assigned a score (0-100%) based on:

Distance to ZLSMA (60% weight): How far the price is from ZLSMA, normalized by ATR. Larger distances indicate stronger breakouts.

Candlestick size (40% weight): The size of the signal candle, normalized by ATR. Larger candles suggest stronger momentum.

A high score (e.g., >80%) indicates a robust signal, while a low score (e.g., <50%) suggests caution.

Visual Features:

The ZLSMA line changes color (green for bullish, red for bearish) to reflect the trend.

Signal candles are highlighted with a subtle green (Buy) or red (Sell) background.

Tiny triangular arrows appear below Buy signals and above Sell signals for clear visual confirmation.

Why Combine Chandelier Exit and ZLSMA?

The Chandelier Exit excels at identifying trend reversals through volatility-based stops, but it can generate false signals in choppy markets due to its sensitivity (especially with a short ATR period of 1). The ZLSMA addresses this by acting as a trend filter, ensuring signals are only triggered when the price confirms a trend by crossing the ZLSMA for the first time. This combination reduces noise and focuses on high-probability setups. The signal strength score further enhances decision-making by quantifying the conviction behind each signal, making the indicator feel intuitive and "smart."

How to Use

Setup:

Add the indicator to your chart in TradingView.

Adjust inputs in the settings panel:

ATR Period (default: 1): Controls the sensitivity of Chandelier Exit. Increase for smoother signals.

ATR Multiplier (default: 2.0): Sets the distance of stop levels from price extremes.

ZLSMA Length (default: 50): Adjusts the smoothness of the ZLSMA line. Shorter lengths (e.g., 20-30) are more responsive; longer lengths (e.g., 50-100) are smoother.

Use Close Price for Extremums (default: true): Determines whether Chandelier Exit uses closing prices or high/low prices for calculations.

Interpreting Signals:

Buy Signal: A green "Buy (X%)" label appears below a candle when the price crosses above the Chandelier Exit short stop and closes above ZLSMA for the first time. The percentage indicates signal strength (higher = stronger).

Sell Signal: A red "Sell (X%)" label appears above a candle when the price crosses below the Chandelier Exit long stop and closes below ZLSMA for the first time.

Use the ZLSMA line’s color (green for bullish, red for bearish) to confirm the overall trend.

Prioritize signals with high strength scores (e.g., >70%) for better reliability.

Trading Considerations:

Combine signals with other analysis (e.g., support/resistance, volume) for confirmation.

Test the indicator on a demo account or use TradingView’s Strategy Tester to evaluate performance.

Be cautious with the default ATR period of 1, as it is highly sensitive and may generate frequent signals in volatile markets.

What Makes It Unique

This indicator stands out due to its thoughtful integration of Chandelier Exit and ZLSMA, creating a synergy that balances sensitivity with reliability. The first-cross filter ensures signals are triggered only at the start of potential trends, reducing false positives. The signal strength score adds a layer of intelligence, helping traders assess the quality of each signal without needing external tools. Visual enhancements, such as dynamic ZLSMA coloring, background highlights, and trend arrows, make the indicator user-friendly and visually engaging, appealing to traders seeking a modern, intuitive tool.

Limitations and Notes

The short ATR period (1) makes the indicator highly sensitive, which suits short-term traders but may produce noise in sideways markets. Increase the ATR period for smoother signals.

The signal strength score is a heuristic based on price movement and momentum, not a predictive model. Use it as a guide, not a definitive predictor.

Always backtest the indicator on your preferred market and timeframe to ensure it aligns with your trading strategy.

MA Crossover [AlchimistOfCrypto]🌌 MA Crossover Quantum – Illuminating Market Harmonic Patterns 🌌

Category: Trend Analysis Indicators 📈

"The moving average crossover, reinterpreted through quantum field principles, visualizes the underlying resonance structures of price movements. This indicator employs principles from molecular orbital theory where energy states transition through gradient fields, similar to how price momentum shifts between bullish and bearish phases. Our implementation features algorithmically optimized parameters derived from extensive Python-based backtesting, creating a visual representation of market energy flows with dynamic opacity gradients that highlight the catalytic moments where trend transformations occur."

📊 Professional Trading Application

The MA Crossover Quantum transcends the traditional moving average crossover with a sophisticated gradient illumination system that highlights the energy transfer between fast and slow moving averages. Scientifically optimized for multiple timeframes and featuring eight distinct visual themes, it enables traders to perceive trend transitions with unprecedented clarity.

⚙️ Indicator Configuration

- Timeframe Presets 📏

Python-optimized parameters for specific timeframes:

- 1H: EMA 23/395 - Ideal for intraday precision trading

- 4H: SMA 41/263 - Balanced for swing trading operations

- 1D: SMA 8/44 - Optimized for daily trend identification

- 1W: SMA 32/38 - Calibrated for medium-term position trading

- 2W: SMA 17/20 - Engineered for long-term investment signals

- Custom Settings 🎯

Full parameter customization available for professional traders:

- Fast/Slow MA Length: Fine-tune to specific market conditions

- MA Type: Select between EMA (exponential) and SMA (simple) calculation methods

- Visual Theming 🎨

Eight scientifically designed visual palettes optimized for neural pattern recognition:

- Neon (default): High-contrast green/red scheme enhancing trend transition visibility

- Cyan-Magenta: Vibrant palette for maximum visual distinction

- Yellow-Purple: Complementary colors for enhanced pattern recognition

- Specialized themes (Green-Red, Forest Green, Blue Ocean, Orange-Red, Grayscale): Each calibrated for different market environments

- Opacity Control 🔍

- Variable transparency system (0-100) allowing seamless integration with price action

- Adaptive glow effect that intensifies around crossover points - the "catalytic moments" of trend change

🚀 How to Use

1. Select Timeframe ⏰: Choose from scientifically optimized presets based on your trading horizon

2. Customize Parameters 🎚️: For advanced users, disable presets to fine-tune MA settings

3. Choose Visual Theme 🌈: Select a color scheme that enhances your personal pattern recognition

4. Adjust Opacity 🔎: Fine-tune visualization intensity to complement your chart analysis

5. Identify Trend Changes ✅: Monitor gradient intensity to spot high-probability transition zones

6. Trade with Precision 🛡️: Use gradient intensity variations to determine position sizing and risk management

Developed through rigorous mathematical modeling and extensive backtesting, MA Crossover Quantum transforms the fundamental moving average crossover into a sophisticated visual analysis tool that reveals the molecular structure of market momentum.

Guntavnook Katta - Price Action PROOverview:

This script is designed to provide traders with a structured, multi-layered view of market behavior. It combines three key components - trend direction analysis, oscillator-based pattern recognition, and projected candle visualization - to help identify meaningful setups and anticipate potential price movements. Additionally, it includes an automated system for plotting multi-level support and resistance zones using swing logic, making it valuable for both discretionary traders and those developing rule-based or semi-systematic frameworks.

Purpose:

The primary purpose of this tool is to empower traders with a structured, multi-dimensional analysis tool that combines both quantitative signals and visual interpretation. Rather than relying on fixed indicators or static strategies, this script allows users to understand the evolving nature of price action through a lens of historical behavior, oscillator dynamics, and market trend context.

It is especially useful for traders who value context-driven decision making - those who prefer to look beyond raw signals and study the sequence of conditions that preceded past price moves, enabling them to better anticipate future possibilities.

Core Logic:

The script brings together three independently developed analytical engines, each built on custom logic and refined through real-market application. Unlike traditional tools that rely on fixed indicator crossovers or rigid rules, this script focuses on pattern dynamics, contextual interpretation, and forward-looking structure - giving it a distinct edge in adapting to different market conditions.

Trend Engine (Volatility-Adjusted Slope Framework):

A moving average alone doesn't reveal much - it’s the slope of the moving average compared against a volatility-normalized threshold that gives meaning. This engine calculates the SMA slope across a user-defined window and dynamically adjusts the threshold using ATR-based volatility. The result: a more adaptive classification of trend into Uptrend, Downtrend, or Sideways, designed to reduce noise and align with real momentum shifts.

Pattern Detection Engine (Zone-Based Signature Matching):

Rather than comparing raw oscillator values, this system maps them into discrete behavioral zones, then tracks their sequential patterns. The most recent pattern is then scanned across historical data to detect exact zone signatures - a method that captures rhythm and structure rather than simple threshold breaks. When a match is found, the script projects what happened next by scaling and rendering those historical candles as projected candle visuals on the current chart - offering a clear and proportionate view of possible price behavior.

Support & Resistance Engine (Tiered Swing-Based Projection):

This module detects significant turning points using user-defined swing lengths, and automatically extends multi-level support and resistance zones (1x, 2x, 3x) into the future. These levels are not based on arbitrary highs/lows, but on tiered confirmation across timeframes, making them highly useful for anticipating potential reaction zones in both trending and consolidating phases.

Together, these components work in sync to offer a layered, context-rich view of price behavior - allowing traders to make better-informed decisions, whether they’re seeking confirmation, confluence, or clarity.

This script is not a signal generator - it is a decision-support tool that allows traders to study market structure in a deeper, more structured way.

It helps answer three essential trading questions:

* What is the current market trend?

* Have similar oscillator-based patterns occurred before, and what followed?

* Where are the likely support and resistance zones based on recent swings?

Key Functional Blocks:

1 - Trend Analysis Using SMA Slope Logic

The script calculates a Simple Moving Average (SMA) over a user-defined period. It compares the slope of this SMA over a second window of candles.

The slope is measured as a percentage and compared against a dynamic threshold derived from price volatility (using ATR).

The market is categorized into:

Uptrend

Downtrend

Sideways

This classification appears in a dedicated trend table at the top-right of the chart, along with the selected oscillator and relevant settings.

2 - Oscillator Pattern Matching Engine

You can select from a variety of studies:

RSI

CCI

Stochastic

Ultimate Oscillator

Money Flow Index

Chande Momentum Oscillator

Relative Volatility Index

The selected oscillator values are converted into different zones. The system continuously monitors the recent pattern of these zones and checks if it matches any past sequence.

Once a historical match is detected:

A message appears in the trend table confirming a match.

The script then activates the projected candle visualization, showing how price behaved after that historical pattern.

3 - Projected Candle Visualization Engine

This feature helps you visualize how price moved historically after a matching oscillator pattern.

How it works:

It retrieves the actual candles that followed the matching pattern in history.

These candles are then scaled relative to the current price to maintain proportional movement.

Candles are drawn using box objects to replicate historical price bars with visual clarity.

Candle color logic is based on oscillator zone at that moment in history -

Green: When the selected oscillator was in an overbought zone (e.g., RSI > 70)

Red: When the selected oscillator was in an oversold zone (e.g., RSI < 30)

Gray: When the selected oscillator was in a neutral zone

This lets traders see:

What happened previously after a similar condition

The general path price followed

Where potential turning points or continuation zones may lie

4 - Multi-Level Dynamic Support & Resistance

Support and resistance levels are drawn based on swing highs and lows across three levels:

You enter an initial swing length (e.g., 10 candles)

The system calculates:

Swing 2 = 2x

Swing 3 = 3x

From there, the indicator detects recent high/low turning points and draws horizontal lines that extend into the future:

R1, R2, R3 (if available) for resistance

S1, S2, S3 (if available) for support

This creates a forward-looking price structure, helping you prepare for reaction zones.

Example Use Cases

Intraday Traders (Best suited for lower timeframes):

This script is particularly effective for intraday traders operating on lower timeframes. It identifies repeating oscillator zone patterns that often precede short-term price movements. When a historical match is found, the projected candles display how price moved in similar situations, offering an immediate visual reference for possible price behavior. Combined with dynamically generated support and resistance zones, the tool adds structure to fast-paced decision-making — helping traders define entries, exits, and stop placements more confidently.

While lower timeframes offer the best responsiveness, the script can be applied across other intraday intervals depending on trading style.

Positional Traders (Best suited for higher timeframes):

For positional traders, this script provides a powerful framework to evaluate whether the current setup mirrors past conditions that led to extended moves. The projected candles show how price evolved after similar oscillator patterns in the past, allowing traders to assess potential directional strength. The trend classification engine and swing-based support/resistance zones further assist in planning position entries, managing holding periods, and identifying key structural levels.

Although higher timeframes offer deeper context for positional trading, the tool remains effective across other multi-day or weekly views as well.

Disclaimer

This script is intended for educational and informational purposes only. It does not provide any form of investment advice, trade recommendations, or performance guarantees. All tools and projections included are meant to support learning and market analysis.

The word “PRO” in the script title refers to a professional-grade analytical tool and should not be interpreted as a claim of profitability or advisory capability.

This script has been developed for use within structured educational environments and is not intended to function as a trading signal or advisory service. Please consult a qualified financial advisor or licensed professional before making any investment decisions.

Pino Trend Pack (SMA/EMA + Bollinger)🔹 Pino Trend Pack is a compact trend-following and volatility indicator that includes:

📈 Moving Averages:

- SMA 10, SMA 30

- EMA 21, EMA 55, EMA 89

(All configured for short-term to mid-term trend analysis by default, but fully adjustable for user preference.)

📊 Bollinger Bands:

- Period: 20

- Standard Deviation: 2.0

- Includes Upper Band, Lower Band, and Basis (SMA 20)

This pack is designed for traders who want a clean visual of price dynamics across multiple short-term trend layers, combined with volatility tracking. It helps you identify compression, expansion, and trend shifts at a glance.

🧠 Ideal for swing trading, short- to mid-term setups, or as a supporting tool in any confluence-based strategy.

Trailing Monster StrategyTrailing Monster Strategy

This is an experimental trend-following strategy that incorporates a custom adaptive moving average (PKAMA), RSI-based momentum filtering, and dynamic trailing stop-loss logic. It is designed for educational and research purposes only, and may require further optimization or risk management considerations prior to live deployment.

Strategy Logic

The strategy attempts to participate in sustained price trends by combining:

- A Power Kaufman Adaptive Moving Average (PKAMA) for dynamic trend detection,

- RSI and Simple Moving Average (SMA) filters for market condition confirmation,

- A delayed trailing stop-loss to manage exits once a trade is in profit.

Entry Conditions

Long Entry:

- RSI exceeds the overbought threshold (default: 70),

- Price is trading above the 200-period SMA,

- PKAMA slope is positive (indicating upward momentum),

- A minimum number of bars have passed since the last entry.

Short Entry:

- RSI falls below the oversold threshold (default: 30),

- Price is trading below the 200-period SMA,

- PKAMA slope is negative (indicating downward momentum),

-A minimum number of bars have passed since the last entry.

Exit Conditions

- A trailing stop-loss is applied once the position has been open for a user-defined number of bars.

- The trailing distance is calculated as a fixed percentage of the average entry price.

Technical Notes

This script implements a custom version of the Power Kaufman Adaptive Moving Average (PKAMA), conceptually inspired by alexgrover’s public implementation on TradingView .

Unlike traditional moving averages, PKAMA dynamically adjusts its responsiveness based on recent market volatility, allowing it to better capture trend changes in fast-moving assets like altcoins.

Disclaimer

This strategy is provided for educational purposes only.

It is not financial advice, and no guarantee of profitability is implied.

Always conduct thorough backtesting and forward testing before using any strategy in a live environment.

Adjust inputs based on your individual risk tolerance, asset class, and trading style.

Feedback is encouraged. You are welcome to fork and modify this script to suit your own preferences and market approach.

Multi-Timeframe MA DashboardThis indicator monitors 5 timeframes: 5min, 15min, 1hr, 4hr, and Daily. It displays fast and slow moving averages for each timeframe, along with the current price. The trend direction is color-coded: green for bullish (fast MA above slow MA) and red for bearish (fast MA below slow MA).

The dashboard also shows the last crossover signal (Buy/Sell) for each timeframe.

Visual arrows are plotted on the chart for the current timeframe. A green up arrow indicates a potential bullish crossover (Buy signal), while a red down arrow indicates a potential bearish crossover (Sell signal).

The dashboard is elegant and professional, with alternating row colors for better readability. It can be placed in any corner of the screen and customized with user-defined colors for bullish and bearish trends.

Alerts are triggered when a crossover occurs on any timeframe. These alerts include the timeframe and signal type (e.g., "5min: ↑ BUY").

How to Read the Indicator

The dashboard displays the following for each timeframe:

Fast MA: The value of the fast moving average.

Slow MA: The value of the slow moving average.

Price: The current price for the timeframe.

Trend: The current trend direction (Bullish or Bearish).

Signal: The last crossover signal (↑ BUY or ↓ SELL).

On the chart, green up arrows indicate a bullish crossover (Fast MA crosses above Slow MA), while red down arrows indicate a bearish crossover (Fast MA crosses below Slow MA).

Green text in the dashboard indicates a bullish trend or signal, while red text indicates a bearish trend or signal.

How to Use the Indicator

Use the dashboard to monitor the trend direction across multiple timeframes. Look for confluence (agreement) between timeframes to identify stronger trends. Observe the "Signal" column in the dashboard for the last crossover on each timeframe. Use the arrows on the chart to identify potential crossover points for the current timeframe.

Enable alerts to be notified of crossover signals on any timeframe. Alerts include the timeframe and signal type for easy reference.

Adjust the fast and slow moving average lengths to suit your trading style. Choose between EMA, SMA, or WMA for the moving average type. Customize the dashboard placement and colors for better visibility.

Important Notes

This indicator is not a buy or sell recommendation. It is a tool to assist traders in their analysis. Always use this indicator in conjunction with other tools, such as support/resistance levels, volume analysis, and price action. Past performance of moving averages does not guarantee future results.

How to Add the Indicator

Add the indicator to your chart from the TradingView library. Configure the inputs:

Fast MA Length: Default is 20.

Slow MA Length: Default is 50.

MA Type: Choose between EMA, SMA, or WMA.

Dashboard Placement: Select the corner of the screen where the dashboard will appear.

Colors: Customize the colors for bullish and bearish trends.

Monitor the dashboard and chart for trends and signals.

Disclaimer

This indicator is for educational and informational purposes only. It does not provide financial, investment, or trading advice. Always perform your own analysis and consult with a financial advisor before making trading decisions.

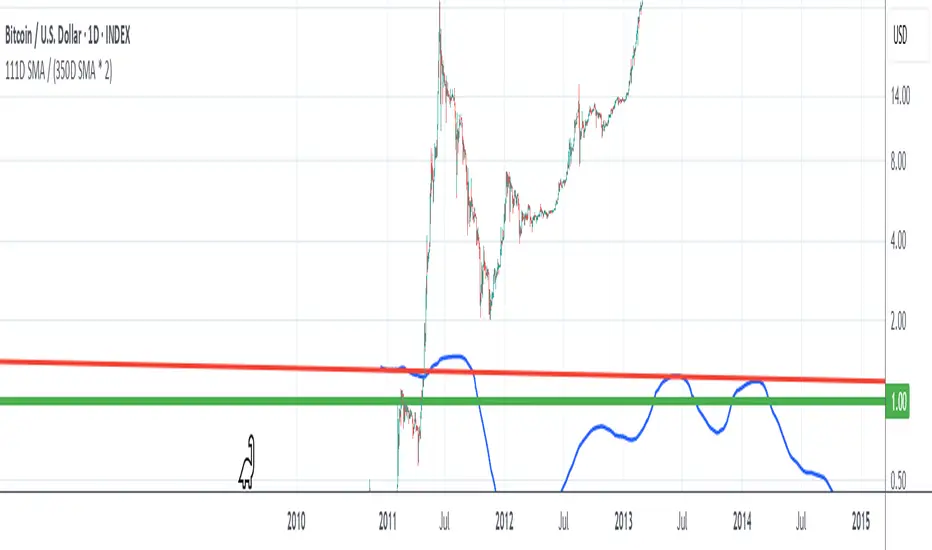

111D SMA / (350D SMA * 2)Indicator: Pi Cycle Ratio

This custom technical indicator calculates a ratio between two moving averages that are used for the PI Cycle Top indicator. The PI Cycle Top indicator triggers when the 111-day simple moving average (111D SMA) crosses up with the 350-day simple moving average (350D SMA *2).

The line value is ratio is calculated as:

Line Value = 111DSMA / (350D SMA × 2)

When the 111D SMA crosses with the 350D SMA triggering the PI Cycle Top, the value of the ratio between the two lines is 1.

This visualizes the ratio between the two moving averages into a single line. This indicator can be used for technical analysis for historical and future moves.

Multi-MA Strategy Analyzer with BacktestMulti-MA Strategy Analyzer with Backtest

This TradingView Pine Script indicator is designed to analyze multiple moving averages (SMA or EMA) dynamically and identify the most profitable one based on historical performance.

Features

Dynamic MA Range:

Specify a minLength, maxLength, and step size.

Automatically calculates up to 20 MAs.

Custom MA Calculation:

Uses custom SMA and EMA implementations to support dynamic length values.

Buy/Sell Logic:

Buy when price crosses above a MA.

Sell when price crosses below.

Supports both long and short trades.

Performance Tracking:

Tracks PnL, number of trades, win rate, average profit, and drawdown.

Maintains individual stats for each MA.

Best MA Detection:

Automatically highlights the best-performing MA.

Optional showBestOnly toggle to focus only on the best line and its stats.

Visualization:

Up to 20 plot() calls (static) for MAs.

Green highlight for the best MA.

Color-coded result table and chart.

Table View

When showBestOnly = false, the table displays all MAs with stats.

When showBestOnly = true, the table displays only the best MA with a summary row.

Includes:

Best MA length

Total PnL

Number of trades

Win rate

Avg PnL per trade

Max Drawdown

Configuration

minLength (default: 10)

maxLength (default: 200)

step (default: 10)

useEMA: Toggle between EMA and SMA

showBestOnly: Focus on best-performing MA only

Notes

MA plotting is static, limited to 20 total.

Table supports highlighting and is optimized for performance.

Script is structured to run efficiently using arrays and simple int where required.

Potential Extensions

Add visual buy/sell arrows

Export stats to CSV

Strategy tester conversion

Custom date range filtering for backtesting

Author: Muhammad Wasim

Version: 1.0

Regime Filter IndicatorRegime Filter – Crypto Market Trend Indicator

📊 Overview

The Regime Filter is a powerful market analysis indicator designed specifically for crypto trading. It helps traders identify whether the market is in a bullish or bearish phase by analyzing key assets in the cryptocurrency market, including Bitcoin (BTC), Bitcoin Dominance (BTC.D), and the Altcoin Market (TOTAL3). The indicator compares these assets against their respective Simple Moving Averages (SMA) to determine the overall market regime, allowing traders to make more informed decisions.

🔍 How It Works

The Regime Filter evaluates three main components to determine the market's sentiment:

1. BTC Dominance (BTC.D) vs. 40 SMA (Medium Timeframe)

The Bitcoin Dominance (BTC.D) is compared to its 40-period SMA on a mid-timeframe (e.g.,

1-hour). If BTC.D is below the 40 SMA, it indicates that altcoins are performing well relative

to Bitcoin, suggesting a bullish altcoin market. If BTC.D is above the 40 SMA, Bitcoin is

gaining dominance, indicating a potential bearish phase for altcoins.

2. TOTAL3 Market Cap vs. 100 SMA (Medium Timeframe)

The TOTAL3 index, which tracks the total market capitalization of all cryptocurrencies except

Bitcoin and Ethereum, is compared to its 100-period SMA. A bullish signal occurs when TOTAL3

is above the 100 SMA, indicating strength in altcoins, while a bearish signal occurs when

TOTAL3 is below the 100 SMA, signaling a potential weakness in the altcoin market.

3. BTC Price vs. 200 SMA (Higher Timeframe)

The current Bitcoin price is compared to its 200-period Simple Moving Average (SMA) on a

higher timeframe (e.g., 4-hour). A bullish signal is given when the BTC price is above the 200

SMA, and a bearish signal when it's below.

🟢 Bullish Market Conditions

The market is considered bullish when:

- BTC Dominance (BTC.D) is below the 40 SMA, suggesting altcoins are gaining momentum.

- TOTAL3 Market Cap is above the 100 SMA, signaling strength in the altcoin market.

- BTC price is above the 200 SMA, indicating an uptrend in Bitcoin.

In these conditions, the background turns green 🟢, and a "Bullish" label is displayed on the chart.

🔴 Bearish Market Conditions

The market is considered bearish when:

- BTC Dominance (BTC.D) is above the 40 SMA, indicating Bitcoin is outperforming altcoins.

- TOTAL3 Market Cap is below the 100 SMA, signaling weakness in altcoins.

- BTC price is below the 200 SMA, indicating a downtrend in Bitcoin.

In these conditions, the background turns red 🔴, and a "Bearish" label appears on the chart.

⚙ Customization Options

- The Regime Filter offers flexibility for traders:

- Enable or Disable Specific SMAs: Customize the indicator by enabling or disabling the 200 SMA for Bitcoin, the 40 SMA for BTC Dominance, and the 100 SMA for TOTAL3.

- Adjust Timeframes: Choose the timeframes for each of the moving averages to suit your preferred trading strategy.

- Real-Time Data Adjustments: The indicator updates in real-time to reflect current market conditions, ensuring timely analysis.

📈 Best Use Cases

- Trend Confirmation: The Regime Filter is ideal for confirming the market's overall trend,

helping traders to align their positions with the dominant market sentiment.

- Trade Entry/Exit Signals: Use the indicator to identify favorable entry or exit points based on

whether the market is in a bullish or bearish phase.

- Market Overview: Gain a quick understanding of the broader crypto market, with a focus on

Bitcoin and altcoins, to make more strategic decisions.

⚠️ Important Notes

Trend-Following Indicator: The Regime Filter is a trend-following tool, meaning it works best in strong trending markets. It may not perform well in choppy, sideways markets.

Risk Management: This indicator is designed to assist in identifying market trends, but it does not guarantee profits. Always apply sound risk management strategies and use additional indicators when making trading decisions.

Not a Profit Guarantee: While this indicator can help identify potential market trends, no trading tool or strategy guarantees profits. Please trade responsibly and ensure that your decisions are based on comprehensive analysis and risk tolerance.

MA SniperThis indicator automatically finds the most effective moving average to use in a price crossover strategy—so you can focus on trading, not testing. It continuously evaluates a wide range of moving average periods, ranks them based on real-time market performance, and selects the one delivering the highest quality signals. The result? A smarter, adaptive tool that shows you exactly when price crosses its optimal moving average—bullish signals in green, bearish in red.

What makes it unique is the way it thinks.

Under the hood, the script doesn’t just pick a random MA or let you choose one manually. Instead, it backtests a large panel of moving average lengths for the current asset and timeframe. It evaluates each one by calculating its **Profit Factor**—a key performance metric used by pros to measure the quality of a strategy. Then, it assigns each MA a score and ranks them in a clean, built-in table so you can see, at a glance, which ones are currently most effective.

From that list, it picks the top-performing MA and uses it to generate live crossover signals on your chart. That MA is plotted automatically, and the signals adapt in real-time. This isn’t a static setup—it’s a dynamic system that evolves as the market evolves.

Even better: the indicator detects the type of instrument you’re trading (forex, stocks, etc.) and adjusts its internal calculations accordingly, including how many bars per day to consider. That means it remains highly accurate whether you’re trading EURUSD, SPX500, or TSLA.

You also get a real-time dashboard (via the table) that acts as a transparent scorecard. Want to see how other MAs are doing? You can. Want to understand why a certain MA was selected? The data is right there.

This tool is for traders who love crossover strategies but want something smarter, faster, and more precise—without spending hours manually testing. Whether you're scalping or swing trading, it offers a data-driven edge that’s hard to ignore.

Give it a try—you’ll quickly see how powerful it can be when your MA does the thinking for you.

This tool is for informational and educational purposes only. Trading involves risk, and past performance does not guarantee future results. Use responsibly.

SMA7 Tail Reversal📌 Description:

The SMA7 Tail Reversal indicator is designed to identify potential counter-trend trading opportunities by checking if candle wicks (tails) respect a key moving average level (SMA7).

This indicator highlights price action where candles are clearly separated from the moving average, suggesting a possible reversal or temporary correction.

📌 How It Works:

Moving Average Calculation:

Calculates a simple moving average (SMA) of length 7 to act as the primary trend filter.

Candle Classification:

Bullish Candle: A candle where the closing price is higher than the opening price, with a short upper wick.

Bearish Candle: A candle where the closing price is lower than the opening price, with a short lower wick.

Conditions for Coloring Candles:

Long Condition (Green Candle):

High & Low are both below the SMA7 line.

Volume is above the 20-period average.

A bullish candle is detected.

Short Condition (Red Candle):

High & Low are both above the SMA7 line.

Volume is above the 20-period average.

A bearish candle is detected.

📌 Visual Representation:

Green Candles: Potential long signals when price action stays below the SMA7 line.

Red Candles: Potential short signals when price action stays above the SMA7 line.

Yellow Line: SMA7, used as the dynamic threshold for signal generation.

📌 Usage:

Best applied to volatile markets with clear trends.

Effective in detecting counter-trend opportunities where price diverges from the SMA7 line.

Works well with additional confirmation tools for better accuracy.

Trend Catcher SwiftEdgeTrend Catcher SwiftEdge

Overview

The Trend Catcher SwiftEdge is a simple yet effective tool designed to help traders identify potential trend directions using two Simple Moving Averages (SMAs). It plots two SMAs based on the high and low prices of the chart, visually highlights trend conditions, and provides buy/sell labels to assist with trade entries. This indicator is best used as part of a broader trading strategy and should not be relied upon as a standalone signal generator.

How It Works

Two SMAs: The indicator calculates two SMAs: one based on the lowest price (Low) and one based on the highest price (High) over a user-defined period (default: 20).

Dynamic Colors:

Green: When the price is above both SMAs (indicating a potential uptrend).

Red: When the price is below both SMAs (indicating a potential downtrend).

Purple: When the price is between the SMAs (indicating consolidation).

The SMAs and the background between them change color dynamically to reflect the current trend condition.

Buy/Sell Labels:

A "Buy" label appears when an entire candlestick (including its low) crosses above both SMAs, marking the start of a potential uptrend.

A "Sell" label appears when an entire candlestick (including its high) crosses below both SMAs, marking the start of a potential downtrend.

To reduce noise, only one label is shown per trend direction. The indicator resets when the price enters the consolidation zone (purple), allowing for a new signal when the next trend begins.

Settings

SMA Length: Adjust the period of the SMAs (default: 20). A longer period smooths the SMAs and focuses on larger trends, while a shorter period makes the indicator more sensitive to price changes.

How to Use

Add the indicator to your chart.

Look for "Buy" labels to consider potential long entries during uptrends (green zone).

Look for "Sell" labels to consider potential short entries during downtrends (red zone).

Use the purple consolidation zone to prepare for potential breakouts.

Always combine this indicator with other forms of analysis (e.g., support/resistance, volume, or other indicators) to confirm signals.

Important Notes

This indicator is a tool to assist with identifying trend directions and potential entry points. It does not guarantee profits and should be used as part of a comprehensive trading strategy.

False signals can occur, especially in choppy or ranging markets. Consider using additional filters or confirmations to improve reliability.

Backtest the indicator on your chosen market and timeframe to understand its behavior before using it in live trading.

Feedback

If you have suggestions or feedback, feel free to leave a comment. Happy trading!

Standard Deviation SMA RSI | mad_tiger_slayerOverview of the Script

The Standard Deviation SMA RSI is a custom TradingView indicator that enhances the Relative Strength Index (RSI) by incorporating a Simple Moving Average (SMA) and Standard Deviation bands . This approach smooths RSI calculations while factoring in volatility to provide clearer trend signals . Additionally, the indicator includes overbought and oversold thresholds, trend-coded RSI signals , and dynamic volatility bands for improved market analysis. This indicator is designed for swing traders and long-term investors looking to capture high-probability trend shifts.

How Do Traders Use the Standard Deviation SMA RSI?

In the provided chart image, the indicator is displayed on a price chart. Each visual component serves a distinct function in identifying trend conditions and volatility levels .

INTENDED USES

⚠️ NOT INTENDED FOR SCALPING

With the smoothing nature of the SMA-based RSI , this indicator is not designed for low-timeframe scalping. It works best on timeframes above 1-hour , with optimal performance in 12-hour, daily, and higher timeframes.

📈 TREND-FOLLOWING & MEAN REVERSION

The Standard Deviation SMA RSI functions as both a trend-following and mean-reverting indicator:

Trend-Following: Identifies strong, sustained trends using RSI signals and SMA confirmation.

Mean Reversion: Detects overbought/oversold conditions based on standard deviation bands and RSI thresholds .

A VISUAL REPRESENTATION OF INTENDED USES

RSI Line (Green/Pink/Gray): The RSI line dynamically changes color based on trend conditions .

Green RSI → Strong uptrend, RSI above the uptrend threshold.

Pink RSI → Downtrend, RSI below the downtrend threshold.

Gray RSI → Neutral state or consolidation.

If the SMA of RSI is above Long Threshold , the market is in a bullish trend.

If it’s below Short Threshold, bearish conditions prevail.

Threshold Lines (Teal/Purple):

Green Line → Long Entry Threshold

Red Line → Short Entry Threshold

Standard Deviation Bands:

Upper Band → Measures bullish volatility expansion

Lower Band → Measures bearish volatility expansion

Colored Candles: Price candles adjust color based on RSI conditions , visually aligning price action with market trends.

Indicator's Primary Elements

Input Parameters

The script includes several configurable settings, allowing users to tailor the indicator to different market environments:

RSI Length: Controls the number of periods for RSI calculations.

SMA Length: Defines the period for the SMA applied to RSI , creating a smoothed trend line.

Standard Deviation Period: Determines the length for volatility calculations.

Overbought and Oversold Levels:

Can be adjusted to customize sensitivity.

Standard Deviation SMA RSI Calculation

The SMA-based RSI smooths fluctuations while the standard deviation bands measure price volatility.

Upper and Lower Bands: Calculated by adding/subtracting standard deviation to/from the SMA-based RSI.

Trend Signal Calculation:

RSI is compared to uptrend and downtrend thresholds to determine buy/sell conditions.

Long and Short Conditions

Buy and sell conditions are determined by RSI relative to key thresholds :

Bullish Signal: RSI above long threshold & SMA confirms trend .

Bearish Signal: RSI below short threshold & SMA confirms downtrend .

Reversals: RSI entering overbought/oversold areas suggests possible trend reversals.

Conclusion

The Standard Deviation SMA RSI is a powerful trend-following and mean-reverting tool , offering enhanced insights into RSI movements, volatility, and market strength . By combining SMA smoothing, standard deviation bands, and dynamic thresholds , traders can better identify trend confirmations, reversals, and overextended conditions .

✅ Customizable settings allow traders to optimize sensitivity.

✅ Works best on high timeframes (12H, Daily, Weekly).

✅ Ideal for swing traders and long-term investors.

Golden Death Cross IndicatorThis indicator uses moving average to detect both a Golden Cross and Death Cross on any timeframe but is recommended for use on the daily and 24 hour timeframes only.

We have also provided instructions on how to create alerts for these indicators below.

Happy Trading!

Moving Averages: We’ll use Simple Moving Averages (SMA). The 50-day SMA looks at the average price over the last 50 periods, and the 200-day SMA does the same for 200 periods.

Crossovers: We’ll check when the 50-day SMA crosses above (Golden Cross) or below the 200-day SMA (Death Cross).

Set Up Alerts

Now, let’s make sure you get notified when a cross happens:

Open the Alerts Menu

On the chart, click the bell icon (top right of the screen) to create an alert.

Configure the Golden Cross Alert

In the “Condition” dropdown, select “Cross Alerts” (the name of your script).

Below that, select “Golden Cross.”

Set “Once Per Bar Close” in the next dropdown (this ensures it only triggers after the period ends, avoiding false signals mid-bar).

Choose how you want to be notified (e.g., popup, email, or phone app—set this under “Notifications”).

Name the alert (e.g., “Golden Cross Alert”) and click “Create.”

Configure the Death Cross Alert

Click the bell icon again to create a second alert.

Condition: “Cross Alerts” > “Death Cross.”

Set “Once Per Bar Close” again.

Choose your notification method.

Name it (e.g., “Death Cross Alert”) and click “Create.”

Smart Investor - Quarterly Earnings by tarunlalwani007OVERVIEW

Smart Investor - Quarterly Earnings displays comprehensive financial data and moving averages directly on your charts. It shows quarterly/yearly earnings alongside customizable moving averages across multiple timeframes, providing both fundamental and technical analysis in one tool.

This tool is designed purely for analysis purposes. No buy or sell recommendations should be made based solely on the information it provides. Always perform your own due diligence and combine multiple sources of information for trading decisions.

FEATURES

Financial Data Analysis

Displays quarterly (FQ) and yearly (FY) financial metrics

Works with both stocks and futures contracts

Customizable metrics with comparison capabilities

Flexible table positioning options

Multi-Timeframe Moving Averages

Daily, Weekly, and Monthly moving averages adapt to chart timeframe

Support for both EMA and SMA with customizable parameters

Color-coded for easy identification of different timeframes

Company Information Display

Information tags for quick company insights

Display key financial metrics and market performance indicators

SME status identification for small/medium enterprises (only for NSE and BSE India)

FNO and lot size information for derivatives

CALCULATION METHODS

Data Sources

Financial metrics (EPS, Sales, Total Shares) are sourced directly from TradingView's financial API

Price data is obtained using appropriate request functions for the current symbol

Header and Tag Calculations

Current Values: All header and tag metrics use the latest available close price

Market Cap: Latest Close Price × Total Outstanding Shares

Free Float Market Cap: Latest Close Price × Free Float Shares

Free Float Percentage: Obtained directly from TradingView financial data

P/E Ratio: Market Cap / TTM Net Income

52-Week Performance:

Down from 52W High: ((Current Close - 52W High) / 52W High) × 100

Up from 52W Low: ((Current Close - 52W Low) / 52W Low) × 100

Table Calculations

Historical Values: Table metrics use price data from the corresponding quarter/year

Quarter-over-Quarter (QoQ) Change: ((Current Value - Previous Quarter Value) / Previous Quarter Value) × 100

Year-over-Year (YoY) Change: ((Current Value - Value from Same Quarter Last Year) / Value from Same Quarter Last Year) × 100

Quarter names are determined based on the current month: Jan/Feb → Dec, Mar/Apr/May → Mar, Jun/Jul/Aug → Jun, Sep/Oct/Nov → Sep. Each quarter is labeled with its end month and year (e.g., "Mar-2024", "Jun-2024").

Moving Average Implementation

Moving Averages: Calculated based on chart timeframe (daily, weekly, monthly)

EMA/SMA: Uses standard formulas with configurable periods

Included with financial data to provide a complete analysis tool in a single indicator

CUSTOMIZATION OPTIONS

Financial Metrics

The following metrics can be selected for both quarterly and yearly tables:

Sales (Revenue)

EPS (Earnings Per Share)

OPM (Operating Profit Margin)

P/E Ratio

PEG Ratio

Free Float (percentage and value)

Market Cap

PAT (Profit After Tax)

Display Options

Comparison Visualization: Percentage mode, dots mode, or combined

Layout: Multiple table positions, adjustable text size

Themes: Light and dark theme support

History: Display up to 8 periods of historical data

Header Information

Company description

Market capitalization

Free float information

Listing year

Return on Equity (ROE)

Industry/Sector classification

Performance relative to 52-week high/low

FNO status and lot size

HOW TO USE

Add the indicator to your chart

Configure the metrics you want to display in the settings

Position the tables where you prefer on your chart

Customize colors and display options

Adjust moving averages to match your trading style

LIMITATIONS

Financial data availability depends on what TradingView provides for each instrument

Some calculations may show NA when underlying data is unavailable

Small market cap stocks or recently listed companies may have limited historical data

Futures contracts are detected automatically but may require manual verification

TECHNICAL NOTES

Automatic futures contract detection with calculation adjustments

SME status determined using an internal database of symbols that is manually maintained and updated

Date handling adjustments near quarter boundaries ensure consistency

All financial data is sourced directly from TradingView's financial API

Company description and sector information comes directly from TradingView symbol data

Smart MA CrossoverThe Smart MA Crossover indicator is a trend-following tool designed to help traders identify high-probability buy and sell signals based on a dynamic moving average and volume confirmation.

This indicator allows traders to customize the moving average type (SMA, EMA, HMA, WMA, VWMA, SMMA, or VWAP) while incorporating an ATR-based filter for better signal clarity.

How It Works

The script analyzes price movements in relation to a selected moving average and volume conditions to generate trend-based trade signals:

🟢 Buy Signal:

- Price is trading above the moving average for at least two bars.

- A sudden upward momentum is detected (price > open * 1.005).

- Volume is higher than the 50-period SMA of volume.

- The price was trading below the moving average three bars ago.

🔴 Sell Signal:

- Price is trading below the moving average for at least two bars.

- A sudden downward movement is detected (price < open * 0.995).

- Volume is higher than the 50-period SMA of volume.

- The price was trading above the moving average three bars ago.

- When these conditions are met, a label appears on the chart, marking the potential trade signal.

Key Features

- Customizable Moving Averages – Choose between SMA, EMA, HMA, WMA, VWMA, SMMA, or VWAP.

- Dynamic Trend Detection – Moving average color changes based on trend direction.

- Volume Confirmation – Avoid false signals by filtering trades using SMA-based volume analysis.

- ATR-Based Signal Placement – Labels are positioned dynamically based on ATR values to improve visibility.

- Background Trend Highlighting – The background changes color depending on whether price is above (green) or below (red) the moving average.

- Alerts for Buy & Sell Signals – Get real-time notifications when a trade signal is generated.

How to Use

- This indicator is best suited for trend-following strategies and works across different markets, including stocks, forex, and crypto.

- It can be used on multiple timeframes, but traders should combine it with additional analysis to refine trade decisions.

- ATR-based signal placement ensures that buy/sell labels do not clutter the chart.

Important Notes

- This indicator does not predict future price movements—it is a trend-based tool meant to assist with trade decisions.

- No financial advice – Always use risk management when trading.

- TradingView users who do not read Pine Script can still fully utilize this script thanks to clear labels and alerts.

Best MA Pair Finder (Crossover Strategy)This indicator automatically identifies the optimal pair of moving averages (MAs) for a crossover strategy using all available historical data. It offers several MA options—including SMA, EMA, and TEMA—allowing users to select the desired type in the settings. The indicator supports two strategy modes: “Long Only” and “Buy & Sell”, which can be chosen via the options.

For each MA pair combination, the indicator performs a backtest and calculates the profit factor, considering only those pairs where the total number of trades meets or exceeds the user-defined "Minimum Trades" threshold. This parameter ensures that the selected optimal pair is based on a statistically meaningful sample rather than on a limited number of trades.

The results provided by this indicator are based on historical data and backtests, which may not guarantee future performance. Users should conduct their own analysis and use proper risk management before making trading decisions.

ROC + SMI Auto Adjust

This indicator combines the Rate of Change (ROC) and the Stochastic Momentum Index (SMI) with automatically adjusted parameters for different time frames (short, medium, long). It normalizes the ROC to match the SMI levels, displays the ROC as a histogram and the SMI as lines, highlights overbought/oversold zones and includes a settings table. Ideal for analyzing momentum on different time frames.

Key Features:

Automatic Parameter Adjustment:

The script detects the current chart time frame (e.g. 1-minute, 1-hour, daily) and adjusts the parameters for the ROC and SMI accordingly.

Parameters such as ROC length, SMI length and smoothing periods are optimized for short, medium and long term time frames.

Rate of Change (ROC):

ROC measures the percentage change in price over a specified period.

The script normalizes the ROC values to match the SMI range, making it easier to compare the two indicators on the same scale.

The ROC is displayed as a histogram, where positive values are colored green and negative values are colored red.

Stochastic Momentum Index (SMI):

SMI is a momentum oscillator that identifies overbought and oversold conditions.

The script calculates the SMI and its signal line, plotting them on the chart.

Overbought and oversold levels are displayed as dotted lines for convenience.

SMI and SMI Signal Crossover:

When the main SMI crosses the signal line from below upwards, it may be a buy signal (bullish signal).

When the SMI crosses the signal line from above downwards, it may be a sell signal (bearish signal).

Configurable Inputs:

Users can use the automatically adjusted settings or manually override the parameters (e.g. ROC length, SMI length, smoothing periods).

Overbought and oversold levels for SMI are also configurable.

Parameter Table:

A table is displayed on the chart showing the current parameters (e.g. timeframe, ROC length, SMI length) for transparency and debugging.

The position of the table is configurable (e.g. top left, bottom right).

How it works:

The script first detects the chart timeframe and classifies it as short-term (e.g. 1M, 5M), medium-term (e.g. 1H, 4H) or long-term (e.g. D1, W1).

Based on the timeframe, it sets default values for the ROC and SMI parameters.

ROC and SMI are calculated and normalized so that they can be compared on the same scale.

ROC is displayed as a histogram, while SMI and its signal line are displayed as lines.

Overbought and oversold levels are displayed as horizontal lines.

Use cases:

Trend identification: ROC helps to identify the strength of the trend, while SMI indicates overbought/oversold conditions.

Momentum analysis: The combination of ROC and SMI provides insight into both price momentum and potential reversals.

Time frame flexibility: The auto-adjustment feature makes the script suitable for scalping (short-term), swing trading (medium-term) and long-term investing.

Trend Zone Moving Averages📈 Trend Zone Moving Averages

The Trend Zone Moving Averages indicator helps traders quickly identify market trends using the 50SMA, 100SMA, and 200SMA. With dynamic background colors, customizable settings, and real-time alerts, this tool provides a clear view of bullish, bearish, and extreme trend conditions.

🔹 Features:

Trend Zones with Dynamic Background Colors

Green → Bullish Trend (50SMA > 100SMA > 200SMA, price above 50SMA)

Red → Bearish Trend (50SMA < 100SMA < 200SMA, price below 50SMA)

Yellow → Neutral Trend (Mixed signals)

Dark Green → Extreme Bullish (Price above all three SMAs)

Dark Red → Extreme Bearish (Price below all three SMAs)

Customizable Moving Averages

Toggle 50SMA, 100SMA, and 200SMA on/off from the settings.

Perfect for traders who prefer a cleaner chart.

Real-Time Trend Alerts

Get instant notifications when the trend changes:

🟢 Bullish Zone Alert – When price enters a bullish trend.

🔴 Bearish Zone Alert – When price enters a bearish trend.

🟡 Neutral Zone Alert – When trend shifts to neutral.

🌟 Extreme Bullish Alert – When price moves above all SMAs.

⚠️ Extreme Bearish Alert – When price drops below all SMAs.

✅ Perfect for Any Market

Works on stocks, forex, crypto, and commodities.

Adaptable for day traders, swing traders, and investors.

⚙️ How to Use: Trend Zone Moving Averages Strategy

This strategy helps traders identify and trade with the trend using the Trend Zone Moving Averages indicator. It works across stocks, forex, crypto, and commodities.

🟢 Bullish Trend Strategy (Green Background)

Objective: Look for buying opportunities when the market is in an uptrend.

Entry Conditions:

✅ Background is Green (Bullish Zone).

✅ Price is above the 50SMA (confirming strength).

✅ Price pulls back to the 50SMA and bounces OR breaks above a key resistance level.

Stop Loss:

🔹 Place below the most recent swing low or just under the 50SMA.

Take Profit:

🔹 First target at the next resistance level or recent swing high.

🔹 Second target if price continues higher—trail stops to lock in profits.

🔴 Bearish Trend Strategy (Red Background)

Objective: Look for shorting opportunities when the market is in a downtrend.

Entry Conditions:

✅ Background is Red (Bearish Zone).

✅ Price is below the 50SMA (confirming weakness).

✅ Price pulls back to the 50SMA and rejects OR breaks below a key support level.

Stop Loss:

🔹 Place above the most recent swing high or just above the 50SMA.

Take Profit:

🔹 First target at the next support level or recent swing low.

🔹 Second target if price keeps falling—trail stops to secure profits.

🌟 Extreme Trend Strategy (Dark Green / Dark Red Background)

Objective: Trade with momentum when the market is in a strong trend.

Entry Conditions:

✅ Dark Green Background → Extreme Bullish: Price is above all three SMAs (strong uptrend).

✅ Dark Red Background → Extreme Bearish: Price is below all three SMAs (strong downtrend).

Trade Execution:

🔹 For longs (Dark Green): Look for breakout entries above resistance or pullbacks to the 50SMA.

🔹 For shorts (Dark Red): Look for breakdown entries below support or rejections at the 50SMA.

Risk Management:

🔹 Use tighter stop losses and trail profits aggressively to maximize gains.

🟡 Neutral Trend Strategy (Yellow Background)

Objective: Avoid trading or wait for a breakout.

What to Do:

🔹 Avoid trading in this zone—price is indecisive.

🔹 Wait for confirmation (background turns green/red) before taking a trade.

🔹 Use alerts to notify you when the trend resumes.

📌 Final Tips

Use this strategy with price action for extra confirmation.

Combine with support/resistance levels to improve accuracy.

Set alerts for trend changes so you never miss an opportunity.

Enjoy!

Maxima MAX1📌 Overview:

This strategy is a Simple Moving Average (SMA) Crossover system with an optional Relative Strength Index (RSI) filter for better trade confirmation. It allows traders to customize key parameters and backtest results within a specific date range.

📊 How It Works:

✅ Entry Conditions:

The closing price must be above both the Fast SMA and Slow SMA.

(Optional) RSI must be above a threshold (default: 50) for additional confirmation.

❌ Exit Condition:

The closing price drops below the Fast SMA, signaling an exit.

🔧 Customizable Inputs:

SMA Lengths: Adjust both Fast and Slow SMA values.

RSI Filter: Enable/disable RSI confirmation with a custom length & threshold.

Backtest Date Range: Choose a start and end date for testing historical performance.

🚀 Why Use This Strategy?

✔ Ideal for trend-following traders looking for momentum-based entries.

✔ Provides an additional RSI filter to reduce false signals.

✔ Helps traders refine their strategy by testing different parameters.

📢 How to Use:

1️⃣ Customize the SMA lengths, RSI settings, and date range.

2️⃣ Enable/Disable the RSI filter as needed.

3️⃣ Analyze historical performance and optimize for different markets.

⚠ Disclaimer:

This strategy is for educational purposes only. Always backtest thoroughly before using it in live trading.

Panic Drop Stock Market Bull/Bear Market Panic Drop Bull/Bear

What It Does:

This indicator identifies bull and bear markets for the S&P 500 (or any stock/index) using the 50-period and 150-period Simple Moving Averages (SMAs). A green background signals a confirmed bull market when the 50 SMA is above the 150 SMA and the 150 SMA slope is flat or upward. A red background signals a confirmed bear market when the 50 SMA is below the 150 SMA and the 150 SMA slope is downward. The background color persists until a new confirmed state is detected, ensuring no gaps—perfect for spotting long-term market trends whether you’re a beginner, trend trader, or long-term investor.

Key Features:

Plots 50 SMA (default: blue line) and 150 SMA (default: orange line).

Background highlights: green for bull markets, red for bear markets.

Persistent background color—no gaps during unconfirmed periods.

Alerts for confirmed bull and bear market transitions.

Fully adjustable: MA periods, slope lookback, and more.

How to Use It:

Add to your S&P 500 chart (e.g., SPX or SPY) on a daily or weekly timeframe (daily default recommended for long-term trends).

Watch for background color changes:

Green background: Confirmed bull market—consider long positions or holding.

Red background: Confirmed bear market—consider shorting or exiting longs.

Customize via settings:

Adjust MA periods (default: 50 and 150).

Set slope lookback (default: 5 bars) to control slope sensitivity.

Change MA colors if desired.

Set alerts: Right-click on the chart > "Add Alert" > Select "Bull Market Confirmed" or "Bear Market Confirmed."

Trade smart: Use the background to confirm market regimes—e.g., go long during green (bull) phases above key support levels, or protect capital during red (bear) phases.

Why It’s Great:

Beginners: Simple background colors make market trends easy to spot.

Trend Traders: 50/150 SMA crossover with slope confirmation catches major market shifts.

Long-Term Investors: Persistent background ensures you stay in the trend without noise.

Created by Timothy Assi (Panic Drop), eToro’s elite investor. Test it, tweak it, and trade with confidence!